HOME BASE

VA Loans 101

Host: Thomas McCormack

Co-Hosts: Judy Horan, Patricia McDerby

Special Guest: Rob Kinney, Gateway Mortgage

Thank You to Our Vets

Thomas McCormack, Broker, Resources Real Estate

Tom McCormack: We all want to thank you if you have served in the US military, including the National Guard and reserves. Thank you for your service. We appreciate the sacrifices made by both you and your family and we are grateful. My name is Thomas McCormack and I am senior partner and co-owner of Resources Real Estate, an independent brokerage in Monmouth County, New Jersey specializing in both residential and commercial real estate. I have been a realtor for over 20 years and am proud to be part of such a caring and skilled group of professionals here at Resources Real Estate. I live in Highlands, New Jersey and manage both our Manasquan and Rumson sales offices.

I am also a founding member of the New Jersey Realtor’s Veterans Presidential Advisory Group, which was established earlier this year to identify the needs of service members and provide support through the home buying process. My colleagues and I were pleased just this last week to participate in the state of New Jersey’s Veterans Day celebration at the PNC Arts Center. And today, as well as every day, we continue to honor the service of all vets, including that of our family members.

And I would like to personally acknowledge the service of my father, Robert McCormack, who served in the US Air Force during the Korean War, and my uncle, Peter McCormack, who also served in the Air Force during the Korean War. And our nephew, Kyle McCormack, who is a captain in the US Army and currently on active duty. And I’d like to introduce my colleagues who are joining us on this call.

First off, Judy Horan is a sales associate and the relocation and referral manager for Resources Real Estate. Hello, Judy.

Judy Horan, Relocation & Referral Manager and Sales Associate, Resources Real Estate

Judy Horan: Hello, Tom, and thanks for inviting me to participate. I just celebrated, as I think my 10 year anniversary of having my real estate license, and I’m based in Rumson’s office of resources real estate. I’ve lived in Monmouth County my entire life. recently 30 years. Eastern Mammoth, specifically Fair Haven, but I actually grew up in Western Mammoth. So, I covered the whole area and I’m happy to do so. Three years ago, I took on the additional role of relocation referral manager, which expanded my real estate knowledge, but also my reach. I cover both nationally and globally.

And I would be remiss if I did not acknowledge and thank wholeheartedly my family members for their service. my dad, a very very proud Marine, Frank Dunn, who proudly served during the Vietnam War, and my father-in-law, John Heran, who, actually fought during World War II. And when he was fighting in France, he was captured and held as a German prisoner of war until he and as he says, he and his fellow prisoners escaped VE Day on May 8th, 1945. the story.Tom McCormack: …

Tom McCormack: Thank you and yes, that is. And Trish McDerby, how you doing today?

As a real estate agent located in Colts Neck in beautiful Monmouth County, I have the privilege of working with individuals and families who are looking to relocate or stay in this wonderful area of New Jersey. I grew up in Rumson and I did not travel very far. I now call Little Silver home. I love our community and I’m so privileged to live in such a beautiful part of New Jersey. I would also like to acknowledge My father was a staff sergeant in the Army Airore during World War II. I have two brothers that served.

My younger brother Timothy was in the US Navy and I couldn’t find a picture of him, so I’m in trouble. and my older brother Tom was a captain, Thomas Brian McDerby. He was a pilot who flew the KC 135 Refuelers. And I am now a proud mother-in-law of Joseph Vandergrift who is with the United States Air Force Security Forces. So I thank all of our vets. Yes.

Tom McCormack: And we thank those who gave that ultimate sacrifice including your brother. Is that correct?

Patricia McDerby: My brother along with his crew sacrificed their own lives after a refueling mission. they veered their plane off saving 250 families that lived in a military complex at Howard Air Force Base in Panama. So I am sadly and proudly a member of a gold star family. So thank you for acknowledging that, Tom.

Tom McCormack: Wow. Thank thats I can’t imagine. our condolences to your family and all gold star families who have experienced that great loss and thank you for their service. at Resources Real Estate this year we really wanted to acknowledge the service of those past and present who are related to our staff and our agents on our social media channels in honor of Veterans Day. It was a small token, small tribute, but one that was meaningful to our company. and this program, Home Base, was created in part to support the efforts of Military on the Move, which is a program created by leading real est a network of the top independent brokerages around the world, of which Resources Real Estate is a member.

And through our membership in Military on the Move, we hope to better address the housing needs of active duty and retired veterans in both rentals and homeownership in the New Jersey counties of Monmouth, Ocean, and Middle Sex. You can learn more about this program at our website resourcesrealestate.com/vets. just so each of our folks here today were certified members of Military on the Move, the program that I just mentioned, and are committed to the utmost professional service with special training to address the unique needs of active duty service members as well as retired vets.

So, you’re in good hands with our colleagues here, Trish, Judy, Bruce Meltzer as well, who was not able to join us, this evening. but each of us have gone through this training and hopefully that will help us to serve, your needs, better. So, today our topic is VA loans. This is truly a great benefit for veterans and we’d like to help our clients and fellow agents better understand how VA loans may be used. So, few basics.

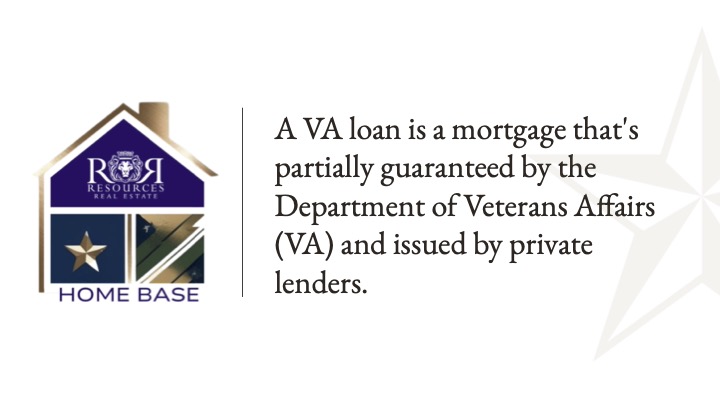

What is a VA Loan?

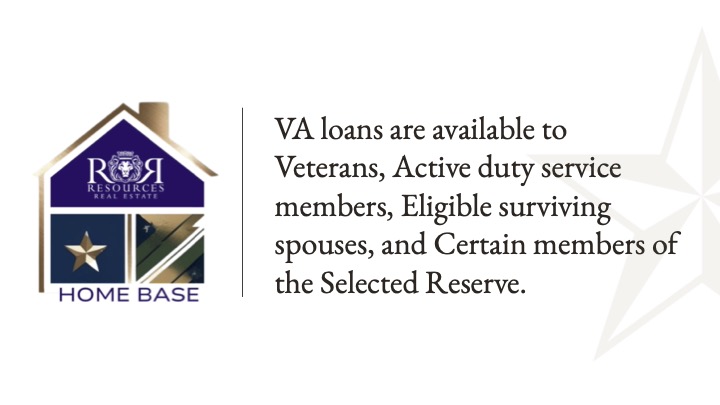

Who is eligible for a VA loan?

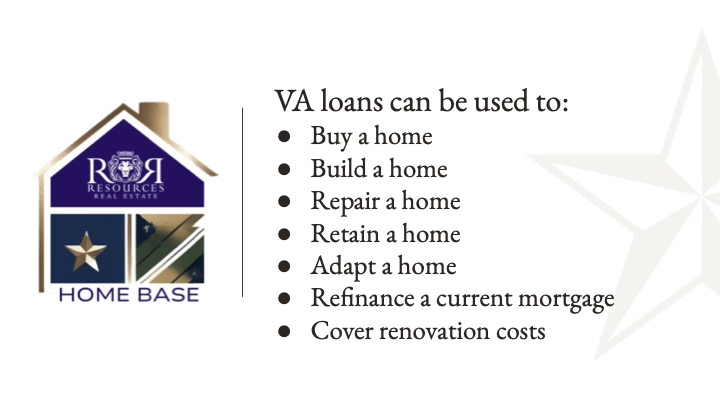

What can a VA loan be used for?

How do you qualify for a VA loan?

Tom McCormack: That’s our quick primer in case you were not familiar with the basics of VA loans, but now we’re very pleased to welcome Rob Kinney, who is sales manager for Gateway Mortgage. His office is right in Red Bank, NJ. Welcome, Rob. We’re very glad to have you join us today to discuss VA loans and other mortgage services available to active duty military and retired vets. And I notice you have a little icon there. seems impressive. What does it mean to be a certified military mortgage advisor?

Rob Kinney: Thanks for having me. a little introduction. Like Tom said, I’m a with Gateway Mortgage. I’ve been doing mortgages around 21 years. located in Red Bank, New Jersey. born and bred in New Jersey, just a little far north of here, and moved down by the shore and never wanted to leave. But, Gateway does have a special program, which I’m really proud of. It’s called Military Mortgage Advisor. So, it specializes in helping out vets with VA loans. They have a special website that you can It answers all your questions. And, obviously, first and foremost, thank you to all the vets out there.

My father-in-law served in Vietnam, and all the vets out there. So, I’m really proud to have this badge to help out veterans because obviously without them, we wouldn’t have a lot of what we have here today. So, it’s a great program. looking forward to, answering any questions, giving a little bit of advice on what the programs are about and helping out. So, I don’t know if we want to dig right into it, but VA loans, it’s a great product. a lot of agents out there, have heard of it, don’t really know much about it. it’s a great program. It’s 100% financing for veterans It’s great that you had the slide up there that shows how you qualify, what you need.

So, if a veteran calls in is asking about a VA loan, there’s a lot of great benefits. again, what we look for is a certificate of eligibility, which basically shows that they’re eligible. If they can’t find it, we would ask them for a DD214 form where we can actually go in and pull their certificate of eligibility for them. also to mention about these loans, there are different products. you can use it for purchases. You can use it as a refinance, which is a streamline refinance, and then a new program out was mentioned before. You can also use it for buying a home and renovating it. So, there’s a lot of great options for vets out there. one of the big things I always like to mention, it’s 100% financing for a reason. it’s to help, vets out. I mean, they deserve, the benefits that we can give them.

So, as an agent a listing agent, right now, especially in this market, that may be looked upon as, not a great loan because they’re not putting any money down. But for the most part, veterans do have money. But if you had an option where you can finance 100% of a home, you get competitive rates, like you have here, flexible credit guidelines, no down payment, there’s no monthly mortgage insurance, it’s a great product for the vets. So don’t just because someone comes to you and has a, 100% financing VA preapproval doesn’t necessarily mean they’re not a qualified buyer.

It’s a great product that they’re taking advantage of. And again, some vets do have money saved that you can show, but it’s a great product. It’s great for vets. And I mean, who wouldn’t take advantage of it?

Tom McCormack: Exactly. And I always say to agents who might be on the receiving end, representing a seller that might be maybe a little bit reluctant. this is a true benefit that has been provided in exchange for their service and we should be honoring that, and not penalizing them. So, thank you for that. Judy, did you want to dig a little deeper?

Judy Horan: The VA loan is a great benefit and one which we’ve used with many of our past clients, but unfortunately not everyone is familiar with this type of mortgage. including real estate agents and even those who qualify for it. So Rob, might you explain this a little bit deeper?

Rob Kinney: Obviously there’s different VA loans. Obviously, it could be used as a purchase, a refinance, and the slide here shows that it’s streamlined. And like I said, to touch base on that, if a veteran wants to refinance, there’s actually a streamline refinance called an Earl. That basically means as long as they’re saving a certain amount of money and a certain amount in the interest rate. There’s no requances on a purchase.

A vet is going to qualify the same way that a normal person would qualify for a mortgage. We, take an application. We do run a credit score. We look at debt, but the credit score requirements are a little lower. The debt ratio requirement, however, on VA loans goes higher. So, that actually allows a vet to qualify for more of a home, especially, in today’s market where home prices are high and interest rates are high. But the best part about VA rates are actually lower right now than conventional rates. So, it’s kind of a win when it comes to a VA loan, whether when you’re purchasing or even refinancing. the other thing too, which was mentioned, was the recent new addition of a renovation loan, which they never had before. we have renovation loans, 203k, Fanny May has a renovation loan. we have a VA renovation loan, which actually will allow a veteran to go in and buy a home and if they need to do a little bit of updating, a little TLC, they can finance in 100% renovation. So, if you have a home that the kitchen’s not done or, you want to, renovate a bathroom, update some stuff about the house, you can actually finance in some money to renovate a home.

So, there’s a lot of different options out there for VA loans. And like it says here, they’re all with basically 0% down. And again, it’s a fantastic option. usually what we’ll do or what’s a nice idea is, if a veteran is taking advantage of the program, you can also basically show proof of assets, meaning, hey, I do have money to use in this, but I want to take advantage of this program because, like I said, 100% financing. You see the screen here. There’s no monthly mortgage insurance, meaning 100% financing with no PMI. You don’t have that on any other program. You don’t have it on conventional, jumbo. This is basically another benefit to the vets out there to say, “Hey, take advantage of this. This program is here for you.

Tom McCormack: That’s you Rob. I’m just curious. Are there any stats that you’re aware of? is the VA loan taken advantage of to the full extent that it could be given the number of vets that are out there?

Rob Kinney: there’s a lot of vets that probably don’t know it even exists. I mean, the majority of them do, and when people call in, they’ll say, I want to want a VA loan. will specifically ask, but some people don’t know that it even is out there, and that could be something that, if a realer is working with a client and they can bring it up, and ask, obviously, younger people,…

Tom McCormack: Yeah, it’s something I’m sorry.

Rob kinney: No, go ahead. I say younger people obviously, but someone who’s a little older, you could say, did you, serve in the armed forces at all? You might be eligible for this fantastic, product where it’s a VA loan.

Tom McCormack: Yeah, I think that I mean for me it’s not a question that I have routinely asked and I think this is really making me think that should be one of the first questions that we ask of an incoming buyer. have you served in any capacity because this could be of tremendous benefit. Trish, I know you wanted to follow up on something Rob was just talking about with the renovation opportunities here.

Patricia McDerby: That’s right. And Rob, you did talk about the renovation loan and rolling it into the initial loan. because as we all know, it’s a tough market out there for buyers because of the limited inventory. And one area that we do see are homes that need renovating. and not everyone is up to the task of undertaking such a project with their own funds. So rolling it into the initial loan is an incredible asset opportunity.

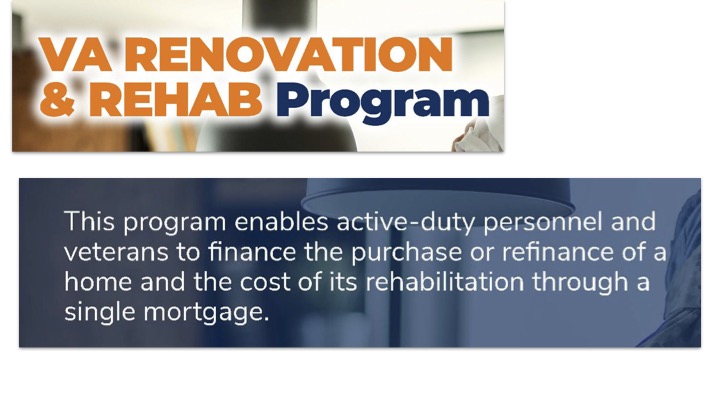

Can a VA loan be used for renovation & rehab properties?

Rob kinney: And it’s really not that hard at all. to talk a little bit about it, if a vet wants to do a renovation loan, just like a regular renovation loan, obviously have a licensed contractor or builder do the work, they do have to be approved by VA, but it’s a very easy way to do it. There’s a couple forms that filled out. They get approved, and they can do this for the vet. the way it works, like all other renovation loans is, again, here you see the slide, you can do it on one to four family homes. condominiums, you can do it on the inside. All condos you have to obviously clear stuff with the association, but it can be done there. It shows here obviously that it’s limited right now to $50,000. So it’s more of someone like I said wants to update or wants to change something around. But the nice part about it is again it’s 100% financing. It’s all done. It’s one closing meaning it’s done from the start. with the contract you have the contractor. That loan is built in.

It goes to closing and then right away basically the contractor will start to get paid to do the renovations. And the nice part about renovation loans is like it says here, there is an after value. So, for example, if a vet’s buying a home and the home is, being bought at $200,000, but he’s going to put $50,000 in there and they’re going to update the kitchens, open up a wall, whatever it might be. The appraiser is going to go out there and say, ” putting this $50,000, this home now is going to be worth, 260, 270, or whatever the end value is. So, there’s sweat equity that, you can actually take advantage. So, it’s a really really great product to use and…

Tom McCormack: So Rob, given that you can use this for multi-family, I presume you have to use this as your primary residence. Is that correct?

Rob kinney: yes, VA loans are only for primary residences. So you would basically be living in the one unit and if it’s a two three family, you would be renting out the other units. And the nice part about that is that for qualification purposes, you can use 75% of the rent to qualify or offset the mortgage. So, if the mortgage, let’s say on a four-unit property, I mean, obviously it’s not going to be cheap.

Let’s say it’s $5,000 a month, but you can get, $1,500 a month rent for the other three units, which is $4,500 per month. They’ll give you 75% of that to offset the mortgage. So, it helps you qualify because they know you’re going to have it rented out. So, multi-units, that’s a benefit of that. But, yes, it’s a great product. Like I said, you do have to live there because it’s only based on, owner occupied homes.

Tom McCormack: And what happens if someone wanted to leave that but still hold on to that property? Would they have to refi out of a VA program for the house that they’re leaving behind if a rental property that they’re leave behind?

Rob kinney: No, you VA loan on that.

Tom McCormack: They could keep it.

Rob kinney: You can rent the other unit out. The only thing that happens though, if you’re buying another home, you can use the VA loan again.

Judy Horan: So heat.

Rob kinney: But what they’ll do is they’ll only let you use rent from the three units that you’ve been receiving for at least two years.

Tom McCormack: This is such a great program.

Rob kinney: So there’s a little bit of a caveat there where …

Patricia McDerby: Yes. Wait, what?

Rob kinney: if a person stays there two years shows that there’s rental income for two years you can use those three units but you can’t use the one that you’re leaving and add that in. but you can reuse a VA loan

Tom McCormack: I mean, I’ve been doing this for over 20 years. I want to really shatter from the rooftops. I mean, this is a real great opportunity for a lot of people. And my guess is that, there’s probably a good number of people that are not fully aware of this being available to them.

Judy Horan: Rob, I’m sorry you’ve sparked a question of mine and now I’m not choking. Sorry about that.

Judy Horan: So how long does it take to get approved for the VA loan? when someone goes in with let’s say, a conventional mortgage, it could be 30 or 45 days or 60. How long does it take to get the funds released for a VA loan approximately? All right.

Rob kinney: It’s the same. There’s no added extra time in underwriting. It’s all done the same because basically what we need up front, somebody calls in and they want a ve and we’re going to ask them upfront. let’s get your certificate of eligibility, let’s get what we need. And once they have that pre-approval, timing wise, it’s the same as any other loan. if we have all their docs, you close in 30 days or even less. So, there’s really downside.

Judy Horan: So it doesn’t hurt because that’s often the question that the seller has is how quickly is this going to hold it up? How quickly can I close?

Tom McCormack: Right. That’s awesome.

Judy Horan: So it’s the same as a conventional really is what you figure. Yeah.

Rob Kinney: Same as conventional. Yeah, you could move as quickly on those as a conventional loan.

Tom McCormack: Thank you, Rob Kinney from Gateway Mortgage. want to share how people can reach out to you if they have any questions. For them to give you a buzz. That’s awesome.

Rob kinney: Yeah, absolutely. My information is there. And also, we actually lend in 42 out of the 50 states. So, I’m not just limited to New Jersey.

Patricia McDerby: Very good.

Rob kinney: So if somebody’s relocating or to a different state I can help them there as well.

Tom McCormack: Thank you, We really do appreciate so on behalf of our Military on the Move sales agents, Judy Haran, Trish McDerby, Bruce Meltzer, we thank you, Rob Kenny from Gateway Mortgage, and all those watching for joining our Homebase program. we hope you have found it helpful. you can watch this and other episodes of Homebase on our Resources Real Estate YouTube channel. And we’re going to be hosting some upcoming episodes which will feature more details about Resources Real Estate’s Military on the Move rebate program which can help you save significantly on real estate commissions. So between your VA loan and that it can substantial savings. and we have somebody who’s just joining us.

I’m just going to let them in. And also just wanted to call your attention to we’ll be talking in future episodes about landlord incentives for veterans housing. There was just some new legislation passed by Governor Murphy that will allow landlords to be incentivized to provide additional housing opportunities for service members and retired vets. And we’re also going to cover in a future episode strategies for home sellers who are vets. so we hope you’ll come back and join us.

I wanted to make sure that you had each of the agents contact information. Any closing thoughts? Judy or Trish? Same here.

Judy Horan: This was a great information session for us as well.

Patricia McDerby: I was just going to say that I learned even more and more about the benefits of VA loans just going through this. And I’ve been taking notes that I have some more questions for our next episode.

Tom McCormack: Thank you everyone for joining us and thank you once again to all of those who are serving currently or have served in the past. Your service is a great gift to us all.

I’m Thomas McCormack, Broker of Resources Real Estate. Thank you for watching Home Base, a program dedicated to bring real estate resources to active duty and retired veterans from Resources Real Estate. You can contact us at 732-212-440 or at our website resourcesrealestate.com or feel free to visit us at any of our sales office locations. We’re conveniently located in Rumson, Colts Neck, Atlantic Highlands, and Manasquan, New Jersey.

Thank you again for joining us. Have a great night and hope to see you at our next episode. Take care.